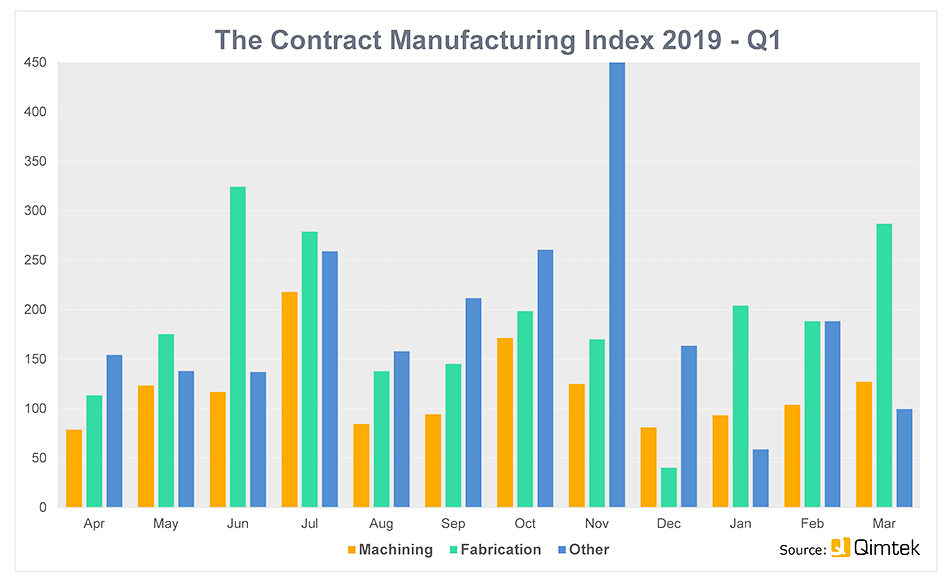

The subcontract market rose 7% in the first quarter of 2019 and is 6% higher than 12 months ago

The UK subcontract manufacturing market continued to grow in the first quarter of 2019, despite a continued lack of resolution on Brexit. According to the latest Contract Manufacturing Index (CMI) figures, business was up 7% in the first three months of 2019 compared to the final quarter of 2018.

There was an upward trend throughout the quarter, compared to a downward trend that had been evident in the last three months of 2018.

Taking a longer-term view, it was also up 6% on the first quarter of 2018 and up by a third since the Brexit vote in the second quarter of 2016.

Within the headline figure, there was a surge in business in the fabrication sector, which was up 66% on the previous quarter, while machining dropped back by 14%.

Overall fabrication accounted for 62% of the value of the market, with machining accounting for 31% and other processes, such as electronics and plastic moulding, accounting for the remaining 7%.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

The baseline figure of 100 represents the average value of the subcontract market between 2014 and 2018. (This has recently been rebased to allow more accurate comparisons of current data and was previously just based on 2014 values.)

Commenting on the figure, Qimtek owner Karl Wigart said: “The latest CMI figures really demonstrate the resilience and underlying strength of UK manufacturing as the subcontract market continues to shrug off the effects of Brexit uncertainty. Many subcontractors are working at full capacity and are even turning work away. The first quarter results show that the dip in the last couple of months of 2018 was a wobble and the index has now climbed back to its normal level.

This strength is driven to a large extent by the fabrication sector where there is a big upswing in work for the medical, scientific, oil and chemical industries.”